Let’s be real here folks, interest rates today are a big deal. Whether you're saving for your dream vacation, paying off student loans, or thinking about buying a house, interest rates play a massive role in how much money ends up in—or out of—your pocket. But what exactly are these rates, and why should you care? Well, buckle up because we’re about to break it down for you in a way that won’t make your eyes glaze over like a glazed donut. Stick with me, and by the end of this, you’ll sound like an economist at your next dinner party.

First things first, interest rates today are basically the cost of borrowing money. Think of it as a fee the bank charges you for letting you use their cash. When rates are low, borrowing becomes cheaper, which is great if you're looking to take out a loan. But when rates go up, it gets more expensive, and that can put a damper on big purchases like cars or homes. So yeah, understanding this stuff is kinda important if you want to keep your finances in check.

Now, I know what you’re thinking—“Why do I need to know all this?” Well, my friend, here’s the thing: interest rates today don’t just affect loans and credit cards. They impact the entire economy, from job growth to inflation. And if you’re smart, you can use them to your advantage. Whether you’re saving, investing, or planning for the future, knowing what’s happening with rates can help you make better financial decisions. So let’s dive in, shall we?

Read also:Car Crash During Spring Break Our Lawyers Can Help

Table of Contents

- What Are Interest Rates?

- Current Interest Rates Today

- Factors Affecting Interest Rates

- How Interest Rates Affect You

- Historical Trends in Interest Rates

- The Central Bank's Role in Setting Rates

- Investing with Interest Rates in Mind

- Saving Strategies During Rising Rates

- Future Predictions for Interest Rates

- Conclusion

What Are Interest Rates?

Alright, let’s start with the basics. Interest rates are essentially the price of borrowing money. If you take out a loan or use a credit card, you’ll likely have to pay interest. On the flip side, if you deposit money into a savings account, you might earn interest. It’s all about supply and demand, my friends. Banks and financial institutions set these rates based on a bunch of factors, including inflation, economic growth, and, of course, the central bank’s policies.

Now, there are different types of interest rates, but the ones you’ll hear about most often are:

- Prime Rate: This is the rate banks charge their best customers. Think of it as the benchmark for other rates.

- Federal Funds Rate: This is the rate banks charge each other for overnight loans. It’s super important because it influences a lot of other rates, including those for consumers.

- Mortgage Rates: These are the rates you’ll see when you’re shopping for a home loan. They tend to be lower than credit card rates but higher than savings account rates.

So why does any of this matter? Because interest rates today can affect everything from your monthly payments to the overall health of the economy. And hey, who doesn’t want to save a buck or two?

Why Understanding Interest Rates Matters

Understanding interest rates today isn’t just for finance nerds. It’s for anyone who wants to make smart financial decisions. For example, if you’re planning to buy a house, knowing whether rates are likely to rise or fall can help you time your purchase. Or if you’re saving for retirement, understanding how rates impact investments can help you grow your nest egg faster.

Current Interest Rates Today

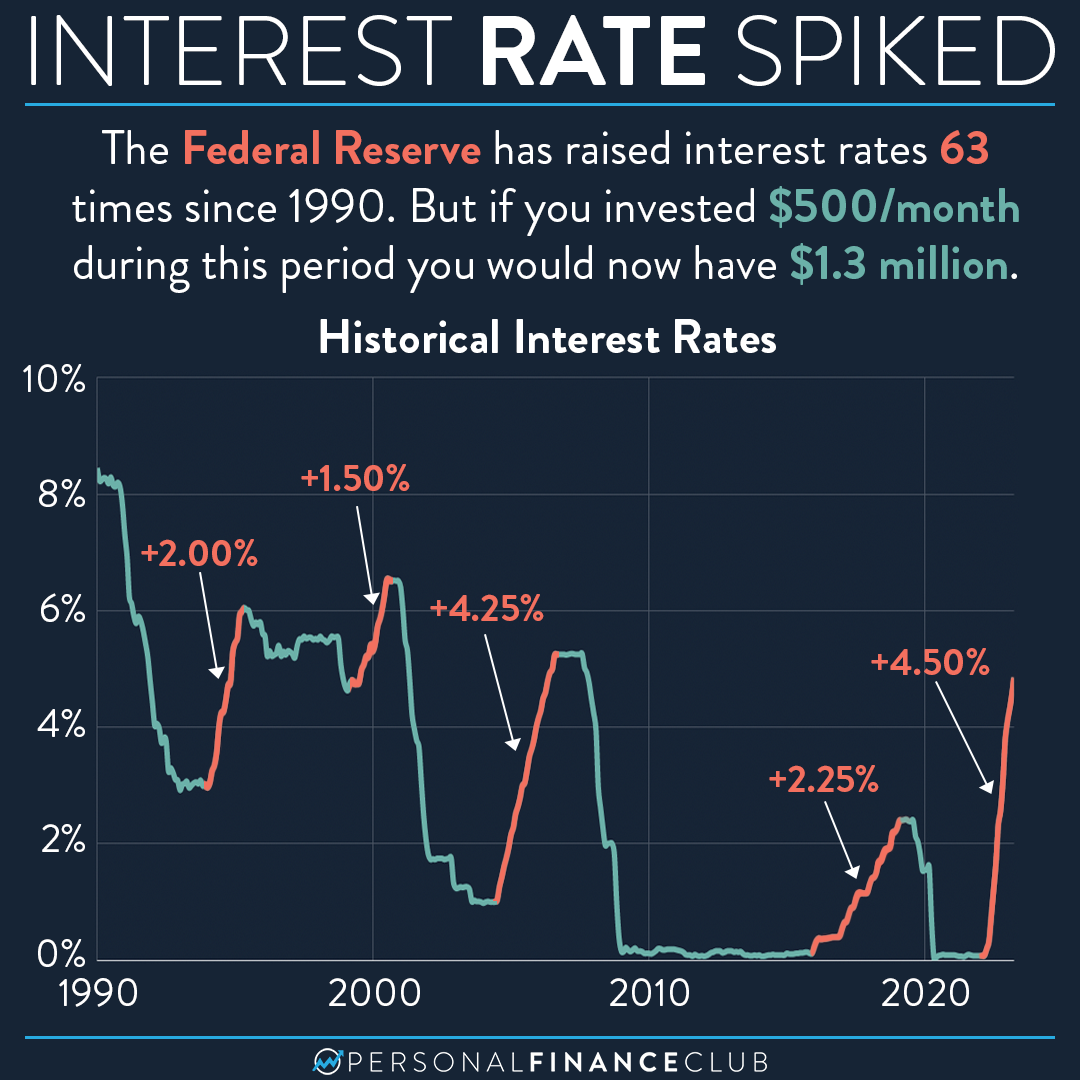

So, what’s actually happening with interest rates today? Well, as of right now, rates are hovering around a certain level, but they’re constantly changing. The Federal Reserve, or the Fed as it’s commonly known, has been adjusting rates to try and keep the economy stable. Inflation has been a hot topic lately, and the Fed’s been raising rates to try and cool things down.

Read also:2023 March Madness Bracket Your Ultimate Guide To The Madness

But don’t just take my word for it. Let’s look at some numbers. According to the latest data from the Federal Reserve, the federal funds rate is currently sitting at [insert current rate]. Mortgage rates are also on the rise, with 30-year fixed rates averaging around [insert rate]. And if you’re thinking about taking out a car loan, expect to pay around [insert rate] in interest.

Key Stats to Keep in Mind

- Federal Funds Rate: [Insert current rate]

- 30-Year Fixed Mortgage Rate: [Insert current rate]

- Average Credit Card APR: [Insert current rate]

Of course, these numbers can fluctuate, so it’s always a good idea to keep an eye on the latest trends. And if you’re feeling overwhelmed, don’t worry—we’ll break it down even further in the next section.

Factors Affecting Interest Rates

Alright, let’s talk about the big picture. What exactly influences interest rates today? Well, there are a ton of factors at play, but here are some of the main ones:

- Inflation: When prices go up, the Fed often raises rates to keep things in check.

- Economic Growth: If the economy is booming, rates might go up to prevent overheating. If it’s slowing down, rates might drop to stimulate growth.

- Global Events: Things like wars, natural disasters, or even pandemics can impact rates by affecting supply chains and consumer confidence.

- Central Bank Policies: As we mentioned earlier, the Fed plays a huge role in setting rates. Their decisions can have a ripple effect across the entire economy.

So, as you can see, there’s a lot that goes into determining interest rates today. And while we can’t control all of these factors, understanding them can help us make smarter financial decisions.

How Global Events Impact Rates

Let’s take a quick look at how global events can affect interest rates today. For example, the pandemic caused a massive disruption in the global economy. In response, the Fed slashed rates to near zero to encourage borrowing and spending. But as the economy started to recover, they began raising rates again to keep inflation in check. It’s a delicate balancing act, and one that can have a big impact on your wallet.

How Interest Rates Affect You

Now, let’s get personal. How do interest rates today actually affect you? Well, it depends on your financial situation. If you’re a borrower, higher rates mean higher monthly payments. But if you’re a saver, higher rates can mean more interest income. It’s a double-edged sword, my friends.

For example, let’s say you have a credit card with a balance of $5,000 and an APR of 18%. If rates go up by just 1%, that could add an extra $50 to your annual interest costs. Ouch. But on the flip side, if you have a savings account with a 2% interest rate and rates go up by 1%, you could earn an extra $20 on a $1,000 deposit. Not bad, right?

Strategies for Borrowers and Savers

Whether you’re borrowing or saving, there are strategies you can use to make the most of interest rates today. For borrowers, consider refinancing loans or transferring credit card balances to take advantage of lower rates. For savers, look for high-yield savings accounts or certificates of deposit (CDs) that offer better returns.

Historical Trends in Interest Rates

Let’s take a quick trip down memory lane. Interest rates today haven’t always been where they are now. In fact, they’ve fluctuated quite a bit over the years. Back in the early 1980s, mortgage rates were sky-high, averaging around 18%. But by the 2000s, they had dropped to historic lows, making it a great time to buy a home.

So what caused these changes? A combination of factors, including inflation, economic growth, and central bank policies. And while we can’t predict the future, looking at past trends can give us a clue about what might happen next.

Lessons from the Past

One thing we can learn from history is that interest rates today are always changing. What might seem like a great deal today could be a bad deal tomorrow. That’s why it’s important to stay informed and adjust your financial strategies accordingly. Whether you’re saving, investing, or borrowing, being adaptable is key.

The Central Bank's Role in Setting Rates

Let’s talk about the Fed for a minute. The Federal Reserve plays a crucial role in setting interest rates today. Through its monetary policy decisions, the Fed tries to keep the economy stable by controlling inflation and promoting employment. But how exactly do they do it?

Well, it’s all about supply and demand. When the economy is overheating, the Fed raises rates to cool things down. When it’s slowing down, they lower rates to stimulate growth. It’s a bit like driving a car—you need to adjust your speed based on the road conditions.

How the Fed’s Decisions Impact You

The Fed’s decisions don’t just affect big banks and corporations. They have a direct impact on your finances too. For example, if the Fed raises rates, you might see higher mortgage payments or credit card interest charges. But if they lower rates, you could see lower borrowing costs or higher savings returns. It’s all interconnected, my friends.

Investing with Interest Rates in Mind

Now, let’s talk about investing. If you’re thinking about putting your money into stocks, bonds, or other assets, interest rates today can play a big role in your decision-making. For example, when rates are low, stocks tend to perform better because borrowing costs are cheaper. But when rates rise, bonds might become more attractive because they offer higher yields.

Of course, there’s no one-size-fits-all strategy. It all depends on your risk tolerance, investment goals, and time horizon. But being aware of how rates impact the market can help you make more informed decisions.

Key Considerations for Investors

Here are a few things to keep in mind when investing with interest rates today in mind:

- Stocks: Generally perform better when rates are low.

- Bonds: Become more attractive when rates rise.

- Real Estate: Can be impacted by changes in mortgage rates.

Saving Strategies During Rising Rates

Finally, let’s talk about saving. If you’re looking to grow your savings during a period of rising interest rates today, there are a few strategies you can use. First, consider switching to a high-yield savings account or CD. These accounts often offer better returns when rates go up, so you can earn more on your deposits.

Another option is to pay down high-interest debt. If you have credit card balances or other loans with high rates, now might be a good time to focus on paying them off. By reducing your debt, you can free up more money for savings and investments.

Tips for Maximizing Savings

Here are a few tips to help you maximize your savings during rising interest rates today:

- Shop around for the best savings account rates.

- Consider laddering CDs to take