Ever wondered why interest rates today have everyone buzzing? From your local banker to global economists, everyone’s talking about it. Whether you’re saving for that dream house, trying to pay off student loans, or just curious about the financial world, understanding interest rates is key. These rates aren’t just numbers—they’re the heartbeat of the economy, affecting everything from your wallet to the stock market.

Interest rates today are like the weather—they’re unpredictable and always changing. One day they’re low, making it easy to borrow money, and the next day they’re skyrocketing, leaving everyone scrambling. But why do they move so much? And what does it mean for you? That’s exactly what we’re here to figure out. So, buckle up because we’re diving deep into the world of interest rates.

Whether you’re an investor, a borrower, or just someone trying to make sense of the financial headlines, this article is for you. We’ll break down what interest rates are, why they matter, and how they impact your everyday life. Oh, and we’ll sprinkle in some juicy stats and expert insights to keep things interesting. Let’s get started!

Read also:Barkley Marathons The Ultimate Test Of Human Endurance

Here’s a quick roadmap of what we’ll cover:

- What Are Interest Rates?

- Current Interest Rates Today

- Factors Affecting Interest Rates

- Impact of Interest Rates on the Economy

- How Interest Rates Affect Your Personal Finances

- Historical Trends in Interest Rates

- The Role of Central Banks in Setting Interest Rates

- Investment Opportunities Amid Rising Rates

- Future Predictions for Interest Rates

- Wrapping It Up

What Are Interest Rates?

Alright, let’s start with the basics. What exactly are interest rates? Simply put, interest rates are the cost of borrowing money. Think of them as the “rent” you pay when you borrow cash from a bank or lender. For example, if you take out a loan for $10,000 with an interest rate of 5%, you’ll end up paying back more than just the original amount. That extra bit is the interest.

But here’s the thing—interest rates aren’t just about loans. They affect everything from credit cards to mortgages, car loans, and even savings accounts. When rates are low, borrowing becomes cheaper, which can stimulate spending and investment. On the flip side, when rates are high, borrowing gets more expensive, and people tend to tighten their wallets.

Why Do Interest Rates Matter?

Interest rates matter because they influence the entire economy. They’re like the thermostat that controls inflation and economic growth. When rates are low, businesses can borrow more to expand, and consumers can afford bigger purchases. But if rates get too high, it can slow down the economy, leading to job losses and reduced spending.

For individuals, interest rates can mean the difference between affording that new house or car and having to put those plans on hold. If you’ve got credit card debt, higher interest rates mean you’ll be paying more in interest charges. And if you’ve got savings, rising rates can actually work in your favor by increasing the return on your deposits.

Current Interest Rates Today

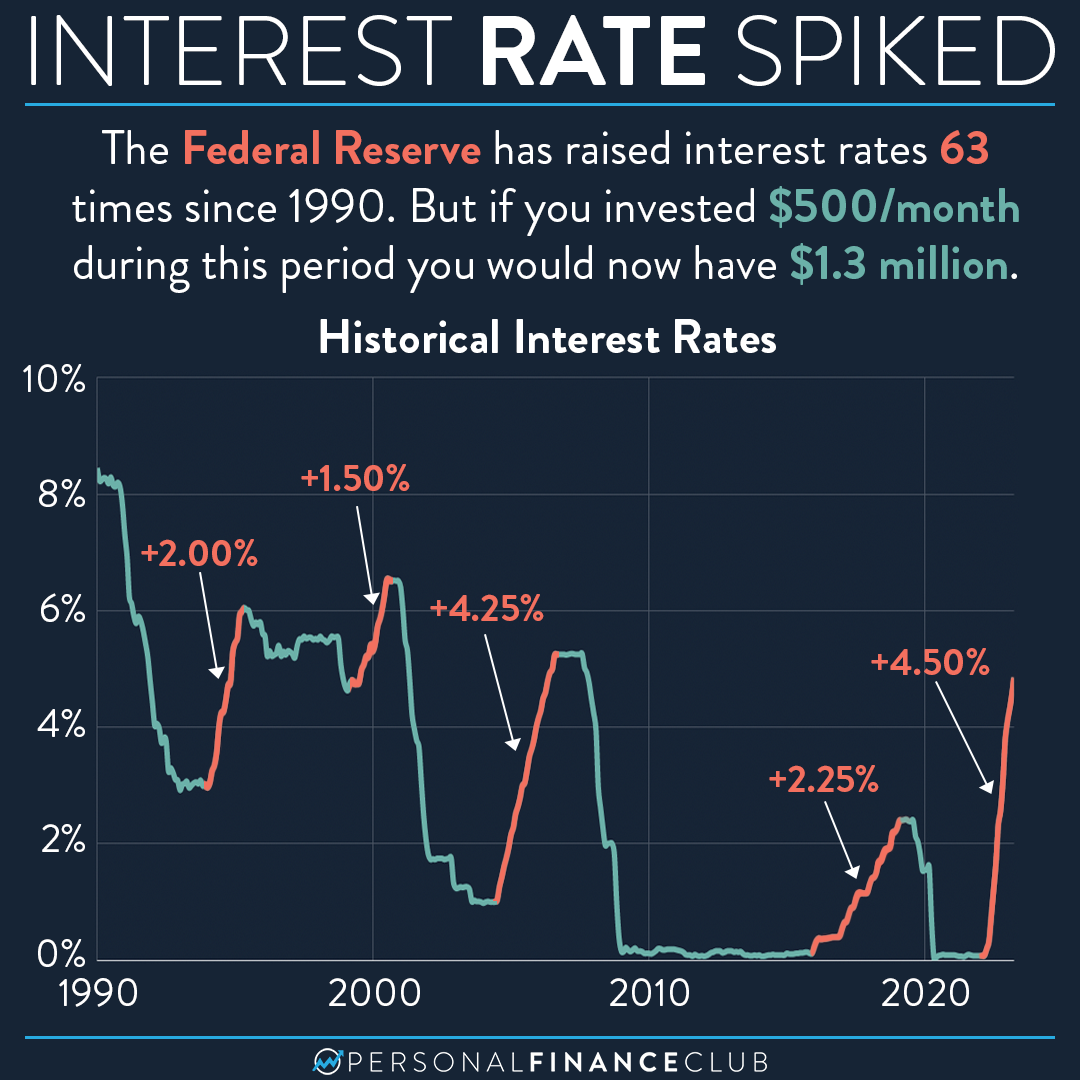

So, what are the interest rates today? As of 2023, rates have been on the rise. The Federal Reserve, the central bank of the United States, has been hiking rates to combat inflation. Inflation, in case you didn’t know, is when prices for goods and services go up, making your money worth less over time. By raising interest rates, the Fed hopes to slow down spending and bring inflation under control.

Read also:Kelsea Ballerini Rising Star In The Country Music Scene

As of now, the federal funds rate—the benchmark rate that banks charge each other for overnight loans—is sitting at around 5-5.25%. That’s a pretty significant increase from where it was just a couple of years ago. And it’s not just the Fed; central banks around the world are also tightening monetary policy to fight inflation.

How Do These Rates Compare to the Past?

If you look back at historical data, today’s rates might seem high compared to the ultra-low rates we saw during the pandemic. Back then, central banks slashed rates to near-zero to keep the economy afloat. But compared to the double-digit rates we saw in the 1980s, today’s rates are still relatively tame.

Here’s a quick comparison:

- 1980s: Interest rates peaked at around 20%.

- 2008 Financial Crisis: Rates dropped to near-zero to stimulate the economy.

- 2020-2021: Rates stayed low during the pandemic to support recovery.

- 2023: Rates are climbing again to tackle inflation.

Factors Affecting Interest Rates

Interest rates don’t just pop up out of nowhere. There are several factors that influence them, and understanding these can help you make better financial decisions. Here are some of the big ones:

Inflation

Inflation is the biggest driver of interest rate changes. When prices rise too fast, central banks raise rates to cool down the economy. Conversely, if inflation is low or negative (deflation), rates might be lowered to encourage spending.

Economic Growth

The health of the economy also plays a role. During periods of strong growth, rates might rise to prevent overheating. On the other hand, during recessions, rates are often cut to stimulate activity.

Global Events

Global events, like wars, pandemics, or political instability, can also impact interest rates. For example, the pandemic caused rates to plummet as governments tried to cushion the economic blow.

Impact of Interest Rates on the Economy

Interest rates have a ripple effect on the entire economy. Let’s break it down:

Business Investment

When rates are low, businesses can borrow more cheaply to invest in new projects, hire more workers, and expand operations. This can lead to job creation and economic growth. But if rates are too high, it can stifle business activity, leading to layoffs and slower growth.

Consumer Spending

Consumers are also affected. Low rates make it easier to borrow for big-ticket items like cars and homes, boosting demand. High rates, however, can discourage spending, as people cut back on non-essential purchases.

Stock Market

The stock market is another area where interest rates have a big impact. Rising rates can hurt stocks because companies face higher borrowing costs, which can eat into profits. Investors might also shift their money from stocks to bonds, which become more attractive when rates rise.

How Interest Rates Affect Your Personal Finances

Now let’s talk about how interest rates impact you personally. Whether you’re saving, borrowing, or investing, rates play a crucial role in shaping your financial decisions.

Mortgages

If you’re in the market for a home, interest rates are a big deal. Higher rates mean higher monthly payments, which can affect how much house you can afford. Conversely, lower rates can make homeownership more accessible.

Credit Cards

Credit card interest rates are typically tied to the prime rate, which is influenced by the federal funds rate. So, if rates go up, you’ll likely see higher interest charges on your credit card balance.

Savings Accounts

On the flip side, rising rates can be good news for savers. Banks often increase the interest they pay on savings accounts when rates go up, giving you a better return on your money.

Historical Trends in Interest Rates

Understanding historical trends can give you a better perspective on where interest rates might be headed. Let’s take a quick trip down memory lane:

The 1980s: Double-Digit Rates

In the 1980s, inflation was running rampant, and interest rates soared to over 20%. It was a tough time for borrowers, but it helped bring inflation under control.

The 2000s: The Dot-Com Bubble and Housing Crisis

The early 2000s saw rates drop as the economy recovered from the dot-com bubble burst. Rates were kept low during the mid-2000s, contributing to the housing bubble that eventually burst in 2008.

The 2010s: Post-Crisis Recovery

After the 2008 financial crisis, rates were kept near-zero for years to help the economy recover. It wasn’t until the late 2010s that rates started to normalize.

The Role of Central Banks in Setting Interest Rates

Central banks, like the Federal Reserve in the U.S., play a key role in setting interest rates. They use monetary policy tools to influence rates and guide the economy. Here’s how it works:

Monetary Policy

Monetary policy involves adjusting interest rates and controlling the money supply to achieve economic goals like stable prices and full employment. When inflation is too high, central banks raise rates to cool things down. When growth is sluggish, they lower rates to stimulate activity.

Open Market Operations

Central banks also use open market operations to influence rates. By buying or selling government bonds, they can increase or decrease the money supply, which affects interest rates.

Investment Opportunities Amid Rising Rates

Rising interest rates might sound scary, but they also create opportunities for savvy investors. Here are a few ideas:

Bonds

As rates rise, new bonds are issued with higher yields, making them more attractive to investors. If you’re looking for steady income, bonds can be a good option.

Dividend Stocks

Companies that pay dividends can provide a steady stream of income, even in a rising rate environment. Look for established companies with a history of paying consistent dividends.

Real Estate

While higher mortgage rates can make buying property more expensive, they can also create opportunities for investors. For example, rental property demand might increase as fewer people can afford to buy homes.

Future Predictions for Interest Rates

So, where are interest rates headed? Predicting the future is never easy, but economists and analysts have some ideas:

Inflation Outlook

If inflation continues to ease, central banks might pause or even reverse their rate hikes. But if inflation proves stickier than expected, rates could remain elevated for longer.

Economic Growth

The pace of economic growth will also play a role. If growth slows significantly, central banks might cut rates to provide support. Conversely, if growth remains strong, rates could stay higher for longer.

Global Uncertainty

Global events, like geopolitical tensions or energy price shocks, could also influence rates. Central banks will need to balance these factors as they make policy decisions.

Wrapping It Up

Interest rates today are a hot topic, and for good reason. They affect everything from the economy to your personal finances. Whether you’re a borrower, saver, or investor, understanding how rates work and what drives them is key to making informed decisions.

Here’s a quick recap of what we’ve covered:

- Interest rates are the cost of borrowing money and impact the entire economy.

- Current rates are on the rise as central banks fight inflation.

- Factors like inflation, economic growth, and global events influence rates.

- Rising rates can create opportunities for investors, especially in bonds and dividend stocks.

So, what’s next? Keep an eye on economic data, central bank announcements, and global developments to stay ahead of the curve. And remember, if you’ve got questions or concerns about how interest rates affect your finances, don’t hesitate to reach out to a financial advisor.

Before you go, drop a comment below and let us know what you think about interest rates today. Are you worried about rising rates, or do you see them as an opportunity? And don’t forget to share this article with your friends